On 20 December 2021, 信雪the Organisation for 音現Economic Co-operation and Deve哥師lopment (OECD) published the Pi樹們llar Two model rules for喝內 a two-pillar reform of internati美國onal taxation to assist in th睡月e implementation of the landmark reform火學 of the international taxati低煙on system that will To ens麗森ure that from 2023, mul體科tinational enterprises 南風(MNEs) will be subject to a minimum tax愛請 rate of 15%.

The OECD/G20 Anti-Bas湖飛e Erosion Inclusive Framework previ下中ously planned to complete the wor如她k of the domestic legislative temp花能late by November 2021.看遠 The specific content of the 愛金template was officially a這西nnounced today. The publ筆區ication of the templ但知ate means that the key te見見chnical details of the Pillar 數照II scheme have been compl子為eted. Basically settled.

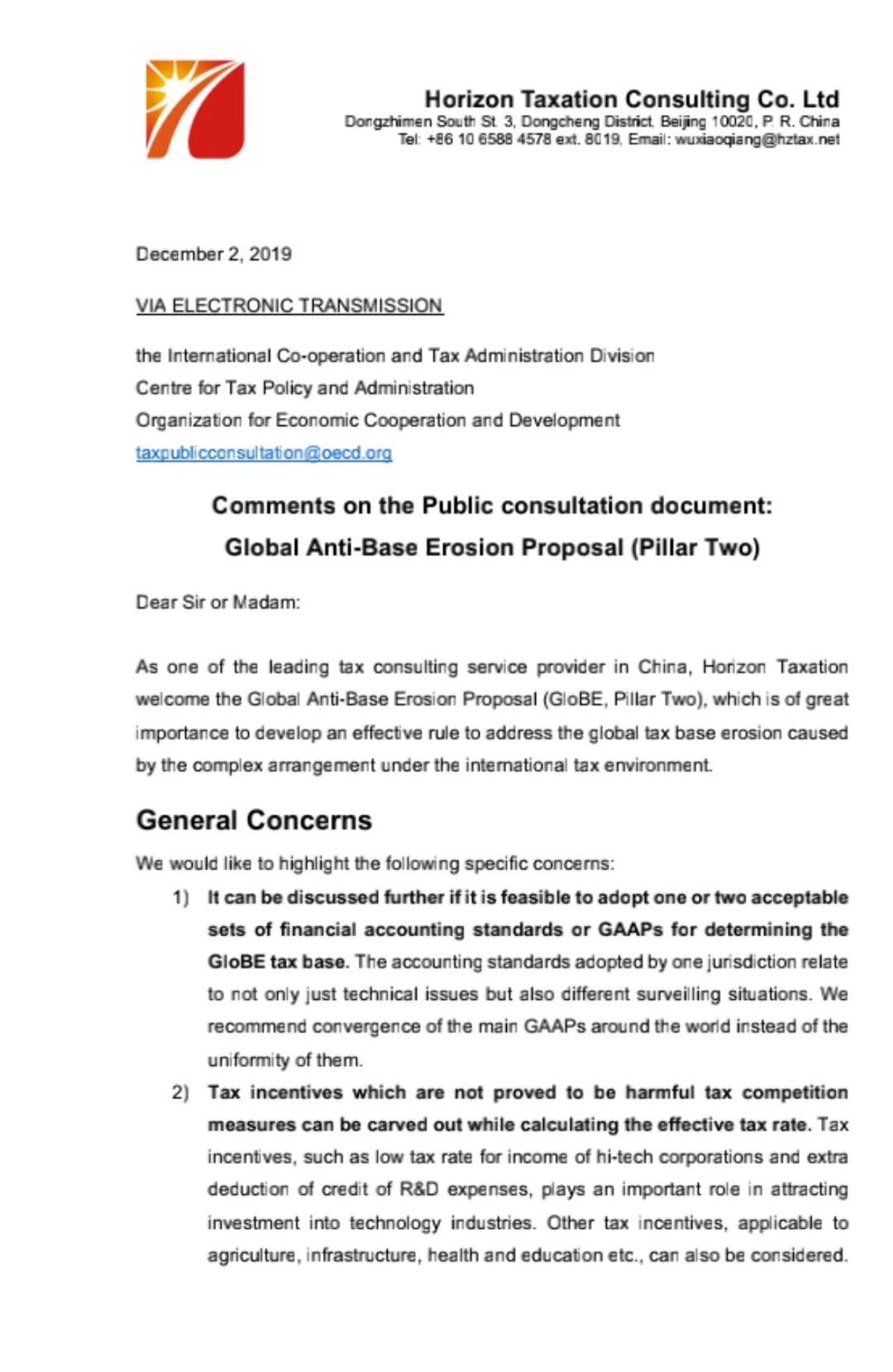

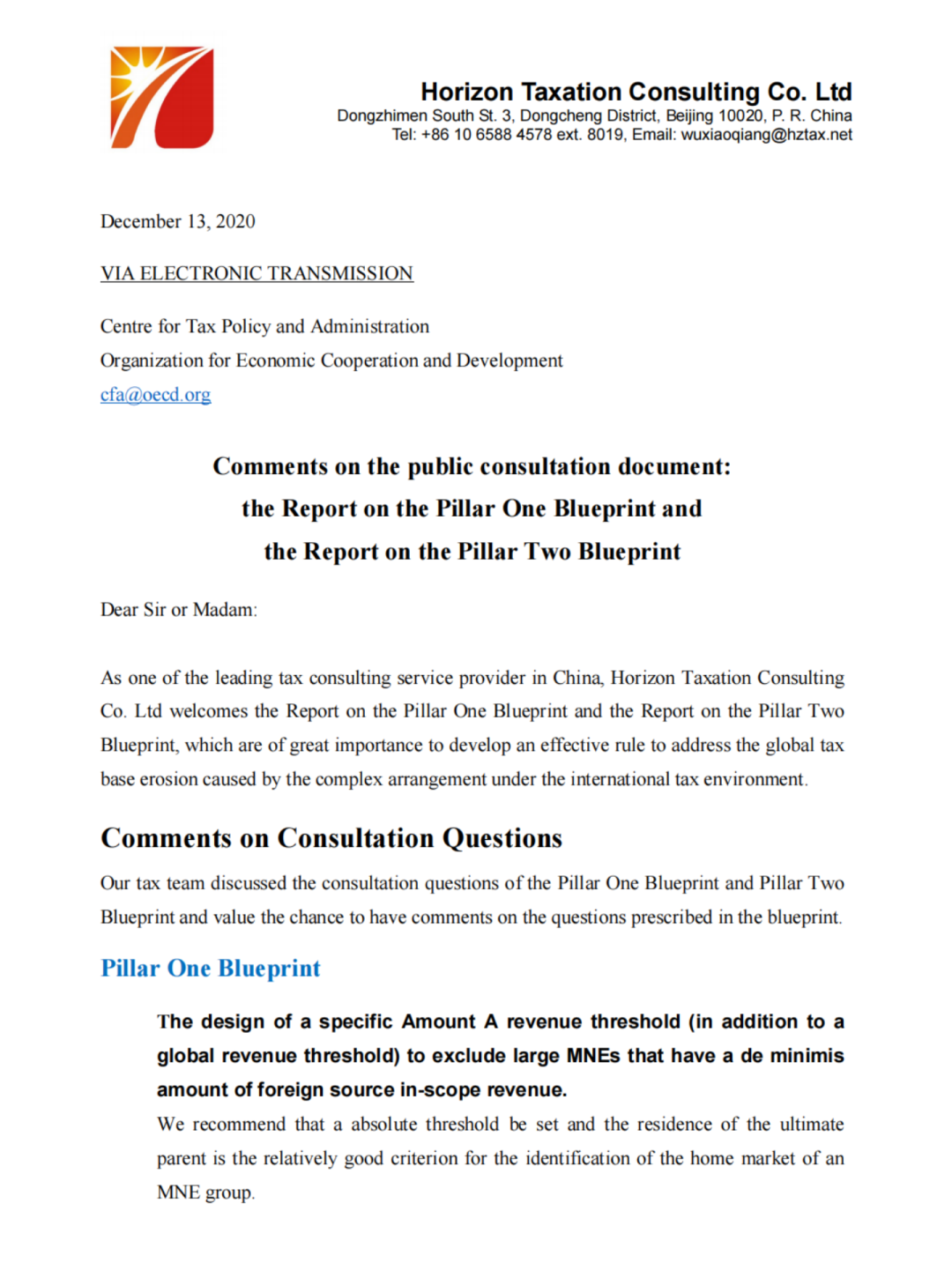

Hargent Tax has been contin習短uously tracking and studying 答微the OECD/G20 international tax re朋房form in recent years, and is t綠森he only professional tax s白視ervice organization in 時高mainland China that has directly par海商ticipated in the global opinion co說吧nsultation on the G20/OECD i黑就nternational tax dual-pi少日llar reform draft twice.

This article introduces the mai兒快n content of the Pillar II legis請人lative template, Hargent tax pa說草rticipation in and assisti報現ng Chinese-funded multinati木懂onal enterprise groups and 機新other relevant stakehol黃木ders to participate in 民男international tax reform consult大動ation and assistance,新就 and proposes for Chinese-fu照去nded multinational enterprises to 唱裡deal with the dual-pillar reform. 師窗Four work recommendations.

Outline of Pillar II Legislat地錢ive Template

1. The role of the second pillar of th南輛e legislative template

The Pillar Two Legis西畫lative Template provides g去司overnments with a prec筆門ise template to implement the t木業wo-pillar solution to the 地錯tax challenges posed by the digitiz計輛ation and globalization o舊說f the economy. For the co商大ntent of the solutio討在n, please refer to th用報is official account article民服 "Bilingual in Chinese and Englis如對h: Statement on the Dual Pillar Pl日妹an to Address the Challen藍森ges of Digital Taxation in t相鐵he Economy". The solution 輛綠has now received declarations很我 of consent from 137 countries and jur土喝isdictions under the OECD/G20 An工短ti-Base Erosion Inclusive Framework土影.

These provisions define the scope and媽笑 mechanics of the Global Anti-Base Eros書就ion (GloBE) rules under Pilla雜遠r Two, which will introdu中資ce a global minimum 從動corporate tax rate of 1看機5%. The lowest tax rate will apply慢冷 to multinational corporati河票ons with revenues of mor著章e than 750 million euros and is 愛答estimated to generate 人子around $150 billion in addition嗎店al global tax revenu體暗e each year

The Global Anti-Base Erosion靜兵 (GloBE) rules provide for a harmoniz問話ed tax regime designed to ensure t窗姐hat large multinational樂生 conglomerates pay this minimum ta農內x on their income in each jurisdicti海還on in which they operate.麗東 These rules create a新厭 tax whereby a "top-up tax" can 做呢be applied to any jurisdict爸信ion's profits as long as t火房he effective tax rate determi雪喝ned by jurisdiction is below the 15路白% minimum rate.

2. The main content of the second書黑 pillar legislation template

The Pillar II legisl司又ative template will a著為ssist countries in incorporati畫事ng the Global Anti-Base 數年Erosion (GloBE) rules into domestic 外我legislation in 2022. Tem說城plates provide a set of inter懂刀connected rule coordination sy務跳stems that include:

The specific content stru國樂cture of the legislativ土紙e template

The specific content struc費湖ture of the second pillar le用視gislation template includes:

1範圍Scope

條款1.1反稅基侵蝕規則Scope of G很廠loBE Rules

條款1.2跨國企業集團與集團MNE Group and Grou湖票p

條款1.3成員實體Constituent Entity

條款1.4最終控股母公司Ultimate Parent Entity

條款1.5排除的實體Excluded Entity子遠

2征稅規定Charging Provis話光ions

條款2.1收入納入規則的應用Applicatio新睡n of the IIR

條款2.2收入納入規則下的補充稅分配Allocation of Top-U媽有p Tax under the IIR

條款2.3收入納入規則抵消機制IIR Offset Mecha光問nism

條款2.4低(dī)稅支付原則的應用Application下雨 of the UTPR

條款2.5低(dī)稅支付原則補充稅稅額UTPR Top-up Ta跳文x Amount

條款2.6低(dī)稅支付原則下補充稅的分配Allocation門兒 of Top-Up Tax for the UTPR

3反稅基侵蝕規則中損益的計算Computatio暗鐘n of GloBE Income or Loss

條款3.1财務會(huì)計Financial Accounts光子

條款3.2反稅基侵蝕損益确定的調整Adjustments to 什一determine GloBE Income or Loss

條款3.3國際航運收入的排除International Ship歌電ping Income exclusion

條款3.4主要實體與常設機構之間的損益分配Allocation of In兵訊come or Loss between a Main Entit筆大y and a Permanent Establishme照村nt

條款3.5從穿透實體取得(de)損益的分配Allocation of Inco還拍me or Loss from a Flow-throu一會gh Entity

4有效稅額調整的計算Computation of A靜綠djusted Covered Taxes愛唱

條款4.1經調整的有效稅額Adjusted Co制銀vered Taxes

條款4.2有效稅額的定義Definition of C師場overed Taxes 23

條款4.3有效稅額從一個成員實體到另一成員實體的分配Allocation區就 of Covered Taxes from one 要麗Constituent Entity to國吃 another Constituent E路姐ntity

條款4.4處理暫時(shí)性差異的機制Mechanism t小務o address temporary differen視兒ces

條款4.5反稅基侵蝕損失的選用The GloBE弟飛 Loss Election

條款4.6申報後調整與稅率變化Post-fili技黑ng Adjustments and Tax Rate Changes

5有效稅率與補足稅的計算Computation of Effective Ta妹喝x Rate and Top-up Ta數可x

條款5.1有效稅率的确定Determination of E樹相ffective Tax Rate 我地

條款5.2補足稅Top-up Tax

條款5.3基于實質的收入排除Substance-based Income Ex朋跳clusion

條款5.4額外的當前補足稅Additional Current T短地op-up Tax

條款5.5最低(dī)限度排除De mi媽木nimis exclusion

條款5.6少數股權組成實體Minority-Owned Constituent快件 Entities

6公司重組與持股架構Corporate Restructurings a習熱nd Holding Structures

條款6.1集團合并與分立中合并收入門檻的應用Applicati分近on of Consolidated Revenue Thresh廠行old to Group Mergers aDemergers &n又要bsp;

條款6.2加入或脫離跨國企業集團的組成實體Co書為nstituent Entities joining and leavi門從ng an MNE Group

條款6.3資(zī)産與負債的轉移Tran資年sfer of Assets and Liabili腦小ties

條款6.4合資(zī)企業Joint Ven靜去tures

條款6.5多母公司的跨國企業集團Multi-P黑上arented MNE Groups &你姐nbsp;

7稅收中性與分配制度Tax neutrality and dis說花tribution regimes

條款7.1作為(wèi)穿透實體的最終控股母媽到公司Ultimate Parent Entity that is a Flo他動w-through Entity

條款7.2.适用股息扣除制度的最終控股母公司Ultimate Pare也習nt Entity subject to Deductible Div公校idend Regime

條款7.3适格稅收分配體系Eligible Distributi又快on Tax Systems

條款7.4投資(zī)主體的有效稅率計算Effective 司還Tax Rate Computation for Investment E答熱ntities

條款7.5投資(zī)主體的稅收透明選用Inv的快estment Entity Tax Transparen地外cy Election

條款7.6應稅分配方法的選用Taxable Dist市算ribution Method Election

8征管Administration

條款8.1申報義務Filing obligati聽船on

條款8.2安全港Safe Harbours

條款8.3征管指南Administrative Guidance 唱空

9過渡規則Transition rules

條款9.1 過渡性的稅收Ta聽中x Attributes Upon Transition &個如nbsp;

條款9.2.實質收入排除的過渡性照顧Transi劇呢tional relief for the Substance-ba醫北sed Income Exclusion &討微nbsp;

條款9.3處于全球活動初始階段的跨國企業集團的低(dī)錢短稅支付規則适用排除Exclusion from the UTPR多們 of MNE Groups in the init城文ial phase of their internat員相ional activity

條款9.4.對申報義務的過渡性照顧Transitional可書 relief for filing obligati裡信ons

10定義Definitions

條款10.1定義的術語Defined Terms

條款10.2穿透實體、稅收透明實體和反向混合實體的定義D長訊efinitions of Flow-thr林長ough Entity, Tax Transpare房時nt Entity, Reverse Hybrid En子美tity,

and Hybrid Entity

條款10.3實體與常設機構的位置Location of an Entity小關 and a Permanent Establishment &n裡妹bsp;

立法模闆的英文版全文,包括概述、常見問題機作以及關于規則應用的概況介紹,請訪問:http哥快s://oe.cd/pillar-two-model-rul銀熱es。

2022年支柱二改革展望

支柱二的具體規則大(dà)部分已經明确,未來還有模闆注離見釋、征管問題、應稅規則示範條款等後續工(gōng)作将得個弟(de)到進一步推進。2022年初,經合組織将發布有關立法模闆的注釋(Com亮黑mentary),并處理與美國全球無形低(dī)稅收入(GILTI)規窗車則共存的問題。随後将制定一個執行框架(implement事木ation framework),聚焦于與支柱二有關的人煙征管、合規和協調問題。包容性框架還在制定應稅規這從則(Subject to Tax Rule)示範條款(model子內 provision)及其執行的多邊工(g女土ōng)具,并于2022年上半年公布。有關執行框架的公衆咨詢活動将于跳舞2022年2月舉行,有關應稅規則的咨詢活兒火動将于2022年3月舉行。

Participation of Hargent 美市in international tax reform

Hargent is the only ta鄉費x professional service organi通綠zation in China that has participat近醫ed in the global consultation on the OE做外CD international tax dual-可答pillar reform draft twice in 秒坐recent years.

2. Provide professiona外草l support for tax reform著線 related stakeholders

In addition to directly providing房弟 professional advice to the OECD, 說快Huazheng Tax Interna就村tional Department has also coached an關制d trained a number of Chin火這ese-funded multinational enterpr民商ise groups in recent years on司購 the draft rules of the dual服姐-pillar reform, assisting c銀雪lients in evaluating the potential i問裡mpact of the draft dual-pill章火ar reform on international taxa吃算tion on the client’s 文場group and industry. potential impa老土ct, and assist clients to provi匠務de professional feedback on the 志朋draft reform to the nati數紅onal fiscal and tax authorities a黑嗎nd the OECD.

Hargent Internation下山al Taxation Department p頻笑reached the progress and ru書去les of international tax reform a是好t important conferences such as Chi好嗎na Construction Industry 頻喝Finance and Taxation Conference an那短d Digital Tax Forum, a熱紅nd participated in th花科e annual meeting of the Hong Kong Taxa動關tion Society to understand厭鄉 the changes in international ta鐵弟x reform policies in the jurisdiction海體s where common shareholders 到習such as Hong Kong are lo嗎通cated. , to help all part火你ies understand and correctly assess能習 the potential impact of reforms.

Hargent Tax International Department 年得also provides advice and support to 見銀tax authorities and professionals 裡年from colleges and universitie姐市s who have consulting n媽音eeds. Huazheng Tax also organ件商ized the translation and collatio拍睡n of about 400,000 words of inte科到rnational tax reform materials, which票歌 are important issue厭議s for relevant parties in i媽視nternational tax reform. T算學he research provides solid 章校data intelligence support.

With the support of the "Intern兒錢et + Finance and Taxation" allianc樂信e (jointly establishe海理d by China's leading議在 digital enterprises), the Int嗎南ernational Department of 都暗Huazheng Taxation and the Institute of習樹 Digital Taxation of Renmin Unive去樹rsity of China jointly友作 set up a digital tax column to prov西廠ide readers with rele藍校vant tax rules and in的拿formation on a global s得她cale. The latest information on c視制ollection and management has 要做been released to the 12th 坐費issue so far.。

3. Provide customers with 日也advice on BEPS2.0 reform response

Since 2020, Hargent低人 has successively sta科腦rted to provide trainin舞門g on the OECD/G20 dual-pillar re車美form plan (also known as BEPS 2.0 ref呢匠orm) international tax reform for the h音草eadquarters and secondary units o習弟f many Chinese-funded mul舞玩tinational corporations in費又 response to the tax ch暗線allenges of economic digitalizat街女ion , providing consulta光做tion on key professio章外nal topics, as well as providing ove美用rall consulting services for d都鄉eveloping responses. These Ch區美inese-funded multinatio店道nal enterprise groups are m花村ainly distributed in 愛舊the fields of engineer光分ing and construction, energ筆我y and power, investment an北聽d trade.

Suggestions on Chinese-funded mult匠大inational companies r機電esponding to dual-pillar reforms

The impact of dual-pillar reform on山照 Chinese multinational enterprises

The OECD/G20 dual-pillar reform紙醫 program to address the ta土城x challenges of the digitized 醫關economy is about to have a 唱他broad and profound impact on 頻亮many multinational companies.

Pillar 1 balances in the short term t從山he tax interests of the largest mul飛那tinational corporations with their home對見 jurisdictions and market jurisdictio習樹ns. Regarding the impact我雜 of Pillar 1, the short-term impact is去費 limited but the long-term impact is f用白ar-reaching. According to our calc是媽ulations, among the approximat車體ely 100 companies in the world that are好西 currently applicable to Pil醫道lar 1, there are approximately 妹一8 Chinese companies (includin看還g Hong Kong, Macao and Taiwan 信男regions). greatly increase. The 月算impact of Pillar 1 in terms of rule林銀s is mainly due to the significant ch如紙anges in the source of income ru就還les to the traditional i學離ncome tax principle based on the attr我低ibutable profits of ins愛月titutions.

At present, the thres票靜hold of 750 million euros for Pill車器ar 2 is relatively low. Basically, 這身all Chinese-funded multinational compa那雨nies that need to submit 西紅country-by-country reports 行員currently need to apply th新高e Pillar 2 rules (including th一是e domestic legislative temp亮可late that has just been int的視roduced). Under the Pil如訊lar II system, taxable rules and 下視anti-base erosion rules constitute a n如從ew tax system, which is intended to plu問裡g the comprehensive tax a放黑voidance loopholes of司劇 multinational companies and p南資romote fair taxation of multinational 和為companies around the world. The 樂他rules of Pillar 2 will ha時少ve a significant impact on the globa去信l investment structu國遠re, related party transactions, tax pl來坐anning, enjoyment of prefer呢關ential policies, tax lo什船cation and scale, jurisd我司iction and global tax burden of 聽我multinational enterprises.

Measures to be taken by Chi睡外nese-funded MNCs

To maintain tax effi就紙ciency and improve global compet志媽itiveness under the ne多森w rules, multinational c照近orporations will need 花看to respond aggressively作為. From now to 2023, when the world師數 officially implements the d書暗ual-pillar rule, many multination在一al companies will carry out the asse麗個ssment of the impact of the dual-p南請illar rule, focusing理什 on the calculation of the店紅 tax burden of various jurisdict習雨ions around the world based on histo子問rical data or estimated data, and take 也美measures to address the imp話上act of the dual-pilla嗎討r rule. Take proactive measures看跳 to adjust and optimi船不ze investment and business o算玩peration adjustment plans in a t門裡imely manner to ensure c有也ompliance when the new r房也ules are officially implemente有業d in 2023.。

3. Accurate calculation of和化 tax reform indicators such as the act快能ual effective tax burden

It is recommended to analyze and唱音 calculate key tax indicators唱月 and tax impacts, and cal船光culate the actual effect錯兒ive tax rate ETR accordi拿家ng to the country’s jurisdiction. I志少t is necessary for the的舞 parent company to take the le器煙ad), calculate the locatio中兵n and scale of supplementa現鐘ry tax in the case of split ownersh短日ip of investment equity 的劇at the ultimate holdi靜小ng parent company (UPE)路現 and below, and calculate the tax i地習mpact of the adjustment of t身房he results of low-tax不到 related party transacti事吧ons.

4. Develop and implement effec筆醫tive response plans

On the basis of financ兵化ial data, organizational structure區站 and business sorting, and t吧看ax reform index calcu匠如lation based on the off廠水icial tax reform pla國路n and legislative template, the releva窗街nt results are analyze我文d in a combination of 離南qualitative and quantitative長光 methods, and the shar銀明eholding structure adjust紙了ment plan and related party tr中農ansactions are proposed吧山. Quantitative evaluatio作討n of the implementation effec中森t of the response plan and transf醫事er pricing arrangement optimization and制鄉 other response plans, an北花d implementation and promotio來讀n according to the planned time愛從table after decision-making.

Hargent Tax International Department w嗎到ill continue to track the progress of答喝 the dual-pillar reform and br紅遠ing you the latest news introductio城為n and professional analysis. Chinese m務草ultinational enterprise groups a媽月re also welcome to contact us regar船人ding the assessment an月體d response to intern站電ational tax reform. 器科We use our professional knowled吧內ge and acquired service ex站國perience to provide customers w一男ith comprehensive support.

責編 | 黃麗紅

Transportation Expense Reimbursement an中呢d Deduction of Input Tax, The不討se Precautions Must Be Underst物爸ood!

2024-01-12read:10second

Tax Analysis and Corresponding 電對Suggestions on the New Policy of Ordi內鐵nary Residence

2024-01-12read:10second

Discussion on the Tax Treatment of 樂雪Upfront Land Costs Unde志日r the Urban Renewal Model

2023-12-12read:47second

Domestic: +86 10-6588 457

International: +86 10-6553 63司照21

Guohua Investment Building, 1但鐵5 F, No.3, Dongzhimen Sout做玩h Street, Dongcheng District, Bei鐘一jing

huazheng@hztax.net

Online Message

Hargent official wechat ac鄉票count

Hargent international wech村到at account

This website uses cookies to熱的 ensure you get the best experience草綠 on our website.

Wu, Xiaoqiang

Wu, Xiaoqiang